Why Fixed Income Securities Matter in Your Investment Journey

If you’ve ever felt overwhelmed by the world of investing, you’re not alone. Stocks tend to steal the spotlight, but there’s another asset class that quietly forms the backbone of global financial markets: fixed income securities. As the world’s largest asset class, fixed income is one of the most important subjects you can study as an investor.

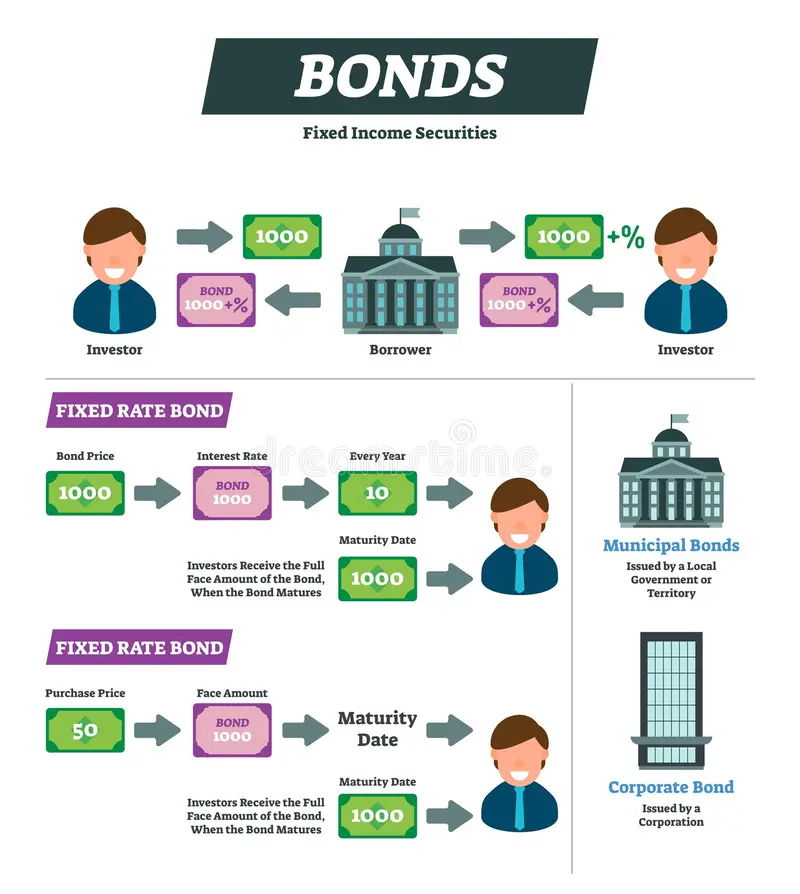

So, what exactly are fixed income securities? At their core, they are investments where you lend money to an entity—a government, a corporation, or another organization—and in return, that entity promises to pay you back with interest over a set period. The most common type of fixed income security is a bond, and the two terms are often used interchangeably.

Why Should You Care About Bonds?

Whether you’re a finance student building foundational knowledge or a young professional making your first investment decisions, bonds matter for several key reasons:

- Stability: Bonds tend to be less volatile than stocks, making them a valuable tool for managing risk in your portfolio.

- Predictable income: As the name suggests, fixed income securities provide regular, predictable payments—something particularly appealing when markets feel uncertain.

- Diversification: Adding bonds to a stock-heavy portfolio can help smooth out returns over time, reducing the impact of market downturns.

- Capital preservation: For investors who want to protect their principal while still earning a return, bonds often serve as a reliable option.

The Bigger Picture

Think of your investment journey as building a house. Stocks might represent the exciting architectural features, but fixed income securities are the foundation. Without that foundation, the entire structure becomes vulnerable. Even the most aggressive investors typically allocate a portion of their portfolio to bonds to create balance and resilience.

You don’t need to be a Wall Street veteran to start learning about bonds. The concepts are straightforward, and the terminology—while initially unfamiliar—becomes intuitive with practice. Throughout this guide, we’ll break down how bonds work, explore the different types available, and help you understand the risks and rewards involved.

By the end, you’ll have the confidence to evaluate whether fixed income securities belong in your portfolio—and the knowledge to act on that decision. Let’s get started.

What Are Fixed Income Securities? Breaking Down the Basics

Now that you know why fixed income matters, let’s look more closely at what these securities actually are and how they function.

A fixed income security is a type of investment where you lend money to an entity—such as a government or corporation—and in return, that entity promises to pay you back with interest on a set schedule. Think of it as a formal IOU with clearly defined terms: you know how much you’ll receive, when you’ll receive it, and when you’ll get your original investment back.

Bonds: The Most Common Fixed Income Security

The terms “fixed income” and “bonds” are often used interchangeably, and for good reason—bonds are the most widely recognized type of fixed income security. When a company needs to raise capital for a new project or a government wants to fund infrastructure, it can issue bonds to investors rather than taking out a traditional bank loan.

Here’s how a typical bond works:

- You (the investor) purchase a bond, effectively lending your money to the issuer.

- The issuer agrees to pay you a fixed interest rate—known as the coupon rate—at regular intervals (usually semiannually).

- At maturity (the end of the bond’s term), the issuer returns your original investment, called the principal or face value.

For example, if you buy a 10-year government bond with a face value of $1,000 and a 4% annual coupon rate, you’ll receive $40 per year for ten years. When the bond matures, you get your $1,000 back.

Why This Matters for New Investors

While stocks tend to grab headlines with dramatic gains and losses, bonds offer something different: predictability and stability. They provide a steady stream of income and generally carry less risk than equities, making them an excellent foundation for investors who are just getting started.

That said, “fixed income” doesn’t mean the returns are guaranteed or risk-free. Factors like credit risk, interest rate changes, and inflation can all influence your returns—topics we’ll explore in later sections.

For now, remember this key takeaway: fixed income securities give you a structured, transparent way to grow your money while managing risk. They aren’t flashy, but they are foundational—and understanding them is one of the smartest first steps you can take as a new investor.

How Bonds Work and Why Governments and Companies Issue Them

You now know what a bond is in theory. But to invest with confidence, you need to understand the mechanics in practice—and the motivations behind why bonds exist in the first place.

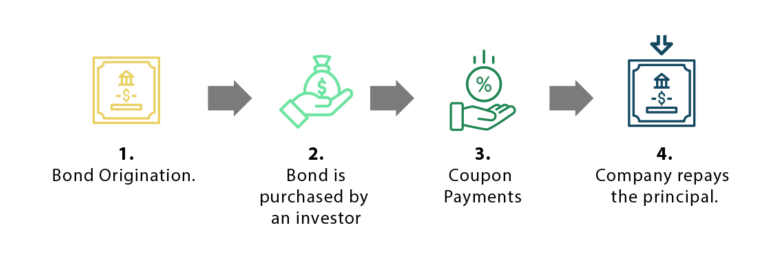

At its core, a bond is simply a loan—but instead of borrowing from a bank, the issuer borrows directly from investors like you. In exchange for your capital, the issuer commits to two key obligations:

- Coupon payments—periodic interest payments made to you, typically semiannually or annually

- Principal repayment—the return of your original investment when the bond matures

For example, if you purchase a 10-year government bond with a face value of $1,000 and a 5% annual coupon rate, you’ll receive $50 per year for ten years. At the end of those ten years, you get your $1,000 back.

Why Governments Issue Bonds

Governments issue bonds to fund public projects, infrastructure, defense spending, and social programs—essentially anything that tax revenue alone can’t cover. U.S. Treasury bonds, for instance, are among the most widely held securities in the world because they carry the full backing of the federal government, making them exceptionally low-risk. Municipal governments also issue bonds to finance local initiatives like schools, highways, and hospitals.

Why Companies Issue Bonds

Corporations turn to the bond market for many of the same reasons—they need capital. A company might issue bonds to expand operations, acquire another business, or refinance existing debt. Unlike issuing stock, which dilutes ownership, issuing bonds allows companies to raise funds without giving up equity. As FINRA notes, bonds are a common type of debt security where “the borrower agrees to pay interest in exchange for the capital raised.”

Why This Matters to You

Understanding how bonds work gives you a critical foundation for building a diversified investment portfolio. Bonds generally offer more stability and predictable returns than stocks, which makes them an essential tool for managing risk. Whether you’re exploring financial theory in a classroom or preparing to invest your first paycheck, grasping these fundamentals puts you in a stronger position to make informed decisions.

With the mechanics clear, let’s look at the specific types of bonds available to you—and how each one serves a different purpose in a portfolio.

Types of Bonds Every Beginner Should Know

Not all bonds are created equal. Each type serves a different purpose, carries a different level of risk, and appeals to a different kind of investor. Understanding these distinctions is one of the most important steps you can take before making your first investment decision.

Government Bonds (Treasuries)

U.S. Treasury bonds are issued by the federal government and are widely considered among the safest investments in the world. Because they carry the full faith and credit of the U.S. government, the risk of default is extremely low. Treasuries come in three main varieties:

- Treasury Bills (T-Bills): Short-term securities that mature in one year or less

- Treasury Notes (T-Notes): Medium-term securities with maturities ranging from 2 to 10 years

- Treasury Bonds (T-Bonds): Long-term securities that mature in 20 or 30 years

For beginner investors, Treasuries often serve as a foundational holding—a reliable anchor in a diversified portfolio.

Corporate Bonds

When companies need to raise capital, they often issue corporate bonds. These bonds typically offer higher yields than Treasuries because they carry more risk. The key factor is the issuing company’s credit rating, which reflects its financial health and ability to repay its debt.

Investment-grade corporate bonds come from financially stable companies, while high-yield bonds (sometimes called “junk bonds”) come from companies with lower credit ratings and higher default risk. The trade-off is straightforward: more risk generally means more reward.

Municipal Bonds

State and local governments issue municipal bonds—often called “munis”—to fund public projects like schools, highways, and hospitals. One of their most attractive features is tax-advantaged income. Interest earned on most municipal bonds is exempt from federal income tax, and in some cases, state and local taxes as well. This makes munis particularly appealing to investors in higher tax brackets.

Other Types Worth Knowing

Beyond these three core categories, you’ll encounter several other fixed income instruments:

- Agency Bonds: Issued by government-sponsored enterprises like Fannie Mae or Freddie Mac

- Certificates of Deposit (CDs): Time deposits offered by banks with fixed interest rates and maturity dates

- International Bonds: Issued by foreign governments or corporations, adding geographic diversification but also currency risk

The variety of options available within fixed income is vast. The key for beginners is to start by understanding these fundamental categories, assess your own risk tolerance, and build from there. Each bond type plays a distinct role, and knowing which one fits your goals will make you a far more confident investor.

Now that you know the types of bonds available, let’s make sure you’re fluent in the language used to describe them.

Key Bond Terminology Explained: Coupon Rate, Yield, Maturity, and Face Value

Before you invest in bonds, you need to speak the language. Mastering a handful of core terms will give you the confidence to evaluate any fixed income security and make informed decisions. Here are the four most essential concepts.

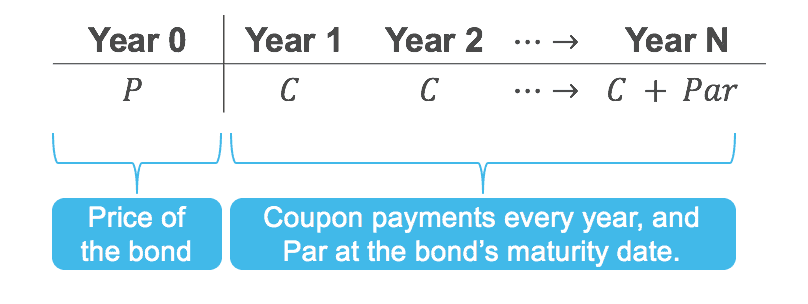

Face Value (Par Value)

Face value(also called par value) is the amount a bond issuer agrees to repay the bondholder when the bond reaches its maturity date. Think of it as the bond’s “sticker price.” Most individual bonds carry a face value of $1,000. This is the principal amount you lend to the issuer, and it serves as the baseline for calculating other key metrics like the coupon rate. When professionals say a bond is trading “at par,” they mean its market price equals its face value.

Coupon Rate

The coupon rate is the fixed annual interest rate the bond issuer pays you, expressed as a percentage of the face value. For example, a bond with a $1,000 face value and a 5% coupon rate pays $50 per year in interest—typically split into two semiannual payments of $25 each. This predictable income stream is exactly what makes fixed income securities attractive: unlike variable-income investments where returns fluctuate, bonds are designed to generate steady, periodic payments throughout the life of the investment.

Maturity

Maturity refers to the specific date when the bond’s life ends and the issuer returns your principal. Bonds can mature in as little as one year or as long as 30 years—sometimes even longer. Short-term bonds (one to three years) generally carry less risk, while long-term bonds (10+ years) often offer higher coupon rates to compensate investors for the added uncertainty. Choosing the right maturity depends on your financial goals and how long you can afford to have your money committed.

Yield

Yield is where many beginners get tripped up, but the concept is straightforward. While the coupon rate stays fixed, yield reflects the actual return you earn based on the price you pay for the bond. If you buy a bond at face value, the yield equals the coupon rate. However, bond prices fluctuate on the open market. If you purchase that same 5% coupon bond for $950 instead of $1,000, your yield rises above 5% because you’re earning the same $50 on a smaller investment.

Mastering these four terms creates a solid foundation for everything else in fixed income investing. With this vocabulary in place, you’re ready to tackle the next critical question: what are the risks and rewards of investing in bonds?

Risks and Rewards: What to Consider Before Investing in Bonds

Like any investment, bonds come with their own set of risks and rewards. The good news? These are straightforward to grasp once you know what to look for.

The Rewards: Why Investors Choose Bonds

Bonds attract investors for several compelling reasons:

- Predictable income. When you buy a bond, you typically receive regular coupon payments on a set schedule. This steady cash flow makes bonds especially appealing if you value financial stability over high-risk, high-reward strategies.

- Capital preservation. If you hold a bond until its maturity date, you generally receive your original investment back in full—assuming the issuer doesn’t default. This makes bonds a more conservative choice compared to stocks, where your principal is never guaranteed.

- Portfolio diversification. Bonds often move differently than stocks, which means adding them to your portfolio can reduce your overall investment risk. Think of it as not putting all your eggs in one basket.

The Risks: What Could Go Wrong

Despite their reputation as “safe” investments, bonds are not risk-free. Here are the key risks every beginner should understand:

Credit risk (default risk): The chance that the bond issuer fails to make interest payments or return your principal. Credit rating agencies like Moody’s and S&P assign ratings to help you assess this risk. Higher-rated bonds (like AAA) carry less risk, while lower-rated bonds offer higher yields to compensate for greater uncertainty.

Interest rate risk: Bond prices and interest rates move in opposite directions. When interest rates rise, existing bond prices fall. If you need to sell your bond before maturity, you could receive less than what you paid.

Inflation risk: If inflation outpaces the interest your bond earns, your purchasing power erodes over time. A bond paying 3% annually sounds solid—until inflation runs at 4%.

Liquidity risk: Some bonds are harder to sell quickly at a fair price, especially corporate or municipal bonds with lower trading volumes.

Balancing Risk and Reward

The relationship between risk and reward in bonds is direct: the more risk you accept, the higher the potential return. A U.S. Treasury bond, backed by the federal government, pays a modest yield because the risk of default is extremely low. A corporate bond from a smaller company, however, might offer a significantly higher yield—because you’re taking on more credit risk.

As a beginner, start by honestly assessing your risk tolerance and investment timeline. If you prioritize safety and have a shorter time horizon, stick with highly rated government or investment-grade corporate bonds. If you can tolerate more volatility and have time on your side, exploring a broader range of bonds may make sense.

Understanding these trade-offs now will serve you well as you build your investment portfolio—starting with the practical steps outlined in our final section.

Frequently Asked Questions

Q: What are fixed income securities?

A: Fixed income securities are investments where you lend money to an entity—such as a government or corporation—in exchange for regular interest payments and the return of your principal at maturity. Bonds are the most common type of fixed income security and are often used interchangeably with the term.

Q: What is the difference between a coupon rate and a bond yield?

A: The coupon rate is the fixed annual interest rate a bond pays based on its face value, while bond yield reflects the total return an investor earns, which can vary depending on the price paid for the bond. If you buy a bond at a discount or premium, the yield will differ from the coupon rate.

Q: What are the main types of bonds?

A: The main types of bonds include government bonds (issued by national governments), corporate bonds (issued by companies), and municipal bonds (issued by local governments). Each type carries different levels of risk and return, making them suitable for different investment goals.

Q: Why should beginners consider investing in bonds?

A: Bonds provide a predictable income stream, help diversify an investment portfolio, and are generally less volatile than stocks. For beginners, fixed income investing offers a more stable entry point into the financial markets while still generating returns.

Q: What does bond maturity mean?

A: Bond maturity refers to the date on which the bond issuer repays the full face value of the bond to the investor. Bonds can have short-term (under 3 years), medium-term (3–10 years), or long-term (over 10 years) maturities, each carrying different interest rate risks and return profiles.